The sort of working class

And a pension abmonination

Hello,

Welcome to Known Unknowns, a newsletter where proper pension accounting makes the world a more beautiful place.

Pension Heresy

I believe there is a painting somewhere that gets uglier every time someone says something outrageously false about pension finance. I guess it is pretty ugly by now, but it got much uglier when Mayor Mamdani released his budget.

Most of the budget gap will be financed by cutting pension contributions by $2.3 billion. I’ve heard many of his allies, and people who just want to think his administration has great economic ideas, argue that this is actually reasonable because the stock market has been so good. Returns were much better than expected, they argue, so the pensions are now overfunded.

Kill me now.

This is what happens when you use an expected return as your discount rate. But even if you think that is reasonable, this is an inane argument. If you think you can underfund when returns are up, that means you need to overfund when returns are down (or just less than you thought they’d be). That also tends to be when New York is in a recession and tax revenues are down.

Now if you pair high returns with a de-risking strategy—say, move the gains into a bond portfolio of appropriate duration—maybe you can justify cutting a contribution here and there. But the pensions aren’t doing this. Instead, they just increased their obligations and are planning on investing in lower-returning, higher-risk assets.

Without de-risking, you are just underfunding.

It goes without saying, but high returns are also not an excuse to cut back on your personal savings. Again, if you de-risk and have a goal, fine. But high returns today (or over the last fifteen years) do not guarantee them tomorrow. Though AI financial advice may say otherwise.

Don’t Work From Home

There was only a two-year period of my career when I was required to be in an office with any regularity. At the time I appreciated the structure and socialization, but it was kind of annoying and time-consuming to have to go somewhere every day and put on nice clothes. Though I still talk to many of my co-workers from then, maybe I’d have more friends and a more fulfilling life if I had more in-office time.

Perhaps that’s why I have always been skeptical of the widespread work-from-home craze. I get that work norms change—people used to work from home before industrialization—but our economy is not suited for it. Too much training and socialization happens at work.

And it turns out, that’s right. Two recent papers estimate that the hiring slowdown of young graduates is not because of AI after all; it is nearly all due to work from home. Remote work makes young staffers more expensive because managing them becomes harder and they get less training.

We blame AI because jobs that adopt the technology are also more likely to be work-from-home amenable. Also, it is tempting to blame AI for everything bad in the economy or our lives. The people behind AI are annoying, the tone of chatbots is annoying, they keep telling us they will take our jobs at best and kill us all at worst. No one is rooting for it, and it’s nice to have a common enemy.

But really, work from home and AI are similar. People who think AI will take all the jobs tend to define a job by a narrow set of tasks that produce output they can easily observe. If you think that’s your whole job, then you can also do it from home. But one thing I learned during my brief foray into office work is that a job is many other things that are harder to observe. Part of that is mentoring and training younger staffers; some of it is contributing to office culture, networking, charming clients, and other soft skills.

Both AI and work from home seem like a cheap fix in the short run, but long term you find it was a false economy.

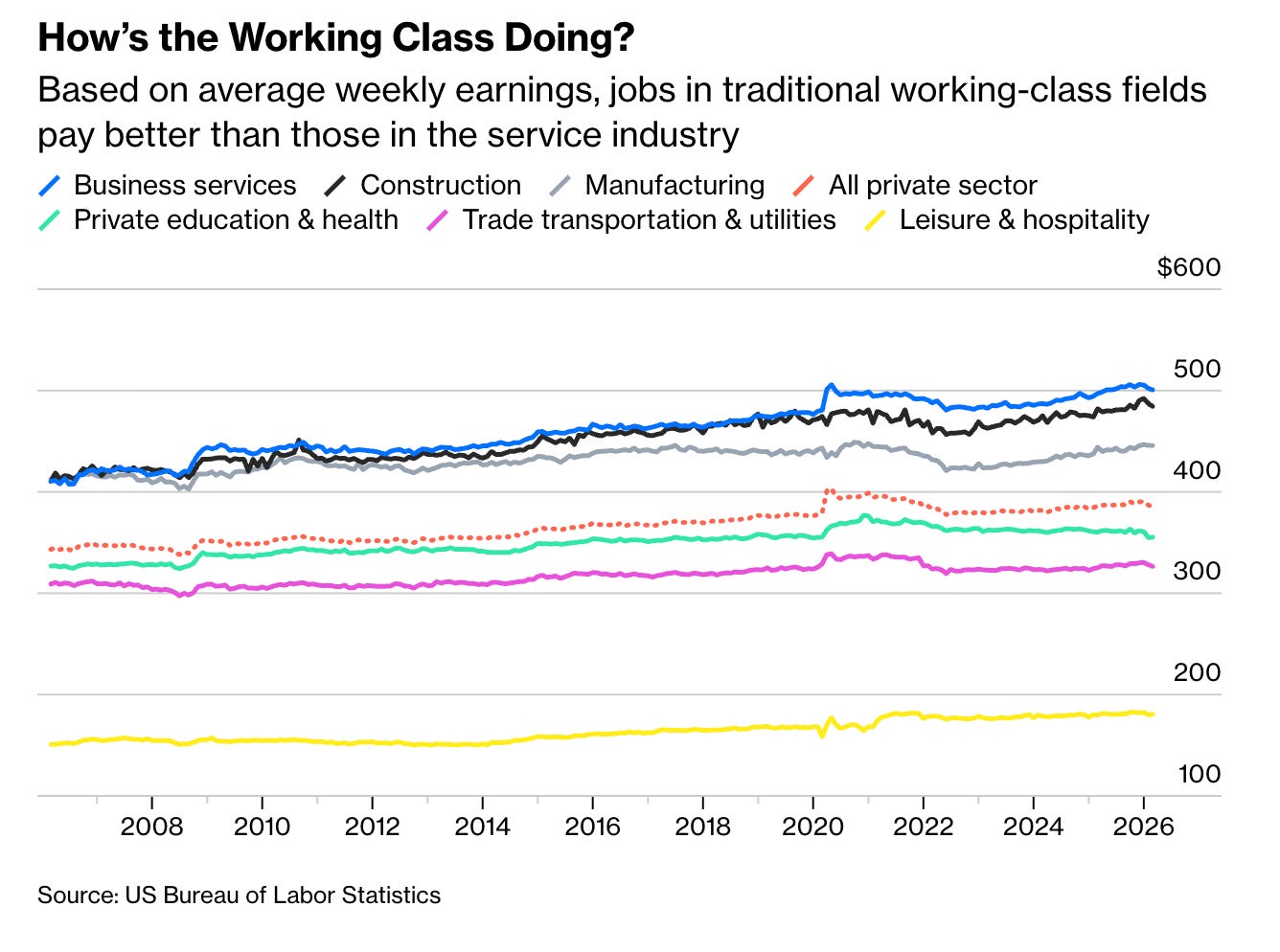

Who Is Working Class?

Graham Platner has some serious problems with both his character and judgment, but he does raise an important question about who is working class today. It is not just an identity; it is a population that wields tremendous political power. And who that population is is always shifting.

Platner thinks working class is anyone who earns a paycheck, but he also says he’s working class and lives mostly off government benefits. But as I think of it, he really is working class.

The working class emerged in the 20th century as a powerful political force, largely through unionization and the many middle-class jobs that manufacturing offered. As manufacturing offered fewer jobs and white-collar work paid much more, working class started to mean underclass—people who needed extra help or were abandoned by policymakers.

But with the latest turn of technology, physical jobs now tend to pay more and seem more secure. The rising underclass contains men who don’t work and collect benefits or money from their families. It also includes people from affluent families who can’t replicate their wealth or lifestyle (often as a result of their own choices).

The latter population is also becoming a potent political force, often running for and winning office. The old working class organized and advocated, but since they also had jobs and were part of the for-profit side of the economy, they had different objectives and well…character.

This may be why the establishment is embracing the leaders of this new coalition, despite some unsavory facts or comments they make.

Until next time, Pension Geeks!

Allison

You understate the remarkable stupidity and ignorance of history when it comes to cutting contributions to public sector defined benefit pension plans - not to mention the use of expected return as the discount rate (rather than, say, a AA muni rate). I'm always amazed when I say to public pension beneficiaries or plan sponsors that discounting future liabilities at the expected return rate implies that their future pension payment are risky (unless the portfolio is all in mix of real return bonds that matches their size and timing, like the Bank of England does). The reply is always the same: "My pension payment isn't risky. It's guaranteed by (e.g., the Illinois state constitution, or my magic ring)". I'm sure that in the minds of public pension beneficiaries, it will be either the bondholders or the US taxpayers who will take the loss if and when the current Ponzi scheme runs out of road. For that reason, the coming public sector pension crisis is a classic "Grey Swan".

No one but the federal government is really in a position to offer defined benefit pensions, so the whole under/over funded issue is a bad take. What KU says about how a defined contribution (deferred compensation) fund should work is of course correct.

Could we please let team managers decide on the optimal trade-off between wage and non-wage (WFH/non-commute) benefits and costs. OMB, CEO’s and media pundits/commentators are not in the best position to judge case by case.