The solutions no one wants to hear

But needs to be said

Photo by Ben Moreland on Unsplash

Hello,

Welcome to Known Unknowns, a newsletter that is having its Jerry Maguire moment this week.

A retirement manifesto

I wrote something of a manifesto for Bloomberg on the state of retirement and what has gone wrong. I hate to say gone wrong because things aren’t terrible. More people than ever have access to some form of a retirement benefit, they have more saved than previous generations, and they have more income. But things could be much, much better.

We feel unprepared because we are saving and investing for wealth when we should be thinking about income. This is not semantics; having the wrong goal results in a less-than-ideal investment strategy, and it is why most people have no idea how much they actually need or how well prepared they are. It also leaves them unprepared to come up with an actual spending plan when they do retire. They also face needless uncertainty, risk, and anxiety. It is not a surprise so many people feel things are off track, even if things are really not so bad.

What upsets me most is these things are relatively easy to fix. We just need new benchmarks that put success in terms of income, some tweaks to our current default investments (to be more income based this means longer duration fixed income), better integration of annuities, and better access to cheap and unbiased advice (and no, expanding the fiduciary standard won’t cut it).

We also need to think differently about work. It seems crazy to me that working longer by raising the normal retirement age further has become so toxic. I am sympathetic to people who have physically grueling jobs and can’t work longer. But we can cover them with disability or dispensations for early retirement. Just because some people can’t retire later doesn’t mean everyone else gets a longer retirement by retiring at the same age and living longer. A better way would be to take a more dynamic approach to work. Reform the labor market so people can do more part-time work as they age. It makes a huge difference for them mentally and financially. By the way, Andrew Scott, who co-wrote The 100-Year Life, has a new book out!

OK, so this all sounds like a lot. But it is all relatively doable. Hurdles exist all over the financial industry, which is rife with conflict and risk aversion, that makes change, even small changes, difficult. I am looking at you, record keepers.

Speaking of, I recall the Secure Act 2.0 required 401(k) statements include income projections—a small step forward, but a good one. I looked at my statements (a few different plans) and this estimate is nowhere to be found.

Living at home

When I wrote about personal finance TikTok, I was struck by how common it was to suggest to twentysomethings that they should live at home with their parents. Not because your life fell apart or you lost your job, just to save money.

source: US Census

It seems like a big change in our social norms. When I was in my 20s, such a thing was unthinkable or a sign there was something wrong with you. Sex and the City even had an episode about it—the man was undatable and a screw-up. But now it is just a way to save money. And I guess that is not wrong, it does save money. But I worry it is a sign of less risk taking and independence. Making the rent is also an important motivator.

True, throughout history people lived at home until they started their own families, and this is a more common thing in Europe (though I am not sure we want to emulate the Italian economy).

It is also notable it is more common for young men than women. Many of them are also not working. It is unclear if living at home in enabling the lack of work or if the lack of work means leaving the nest is harder. In this tight labor market, I think it is the former. These are important years for skill and social development—you don’t get that time back.

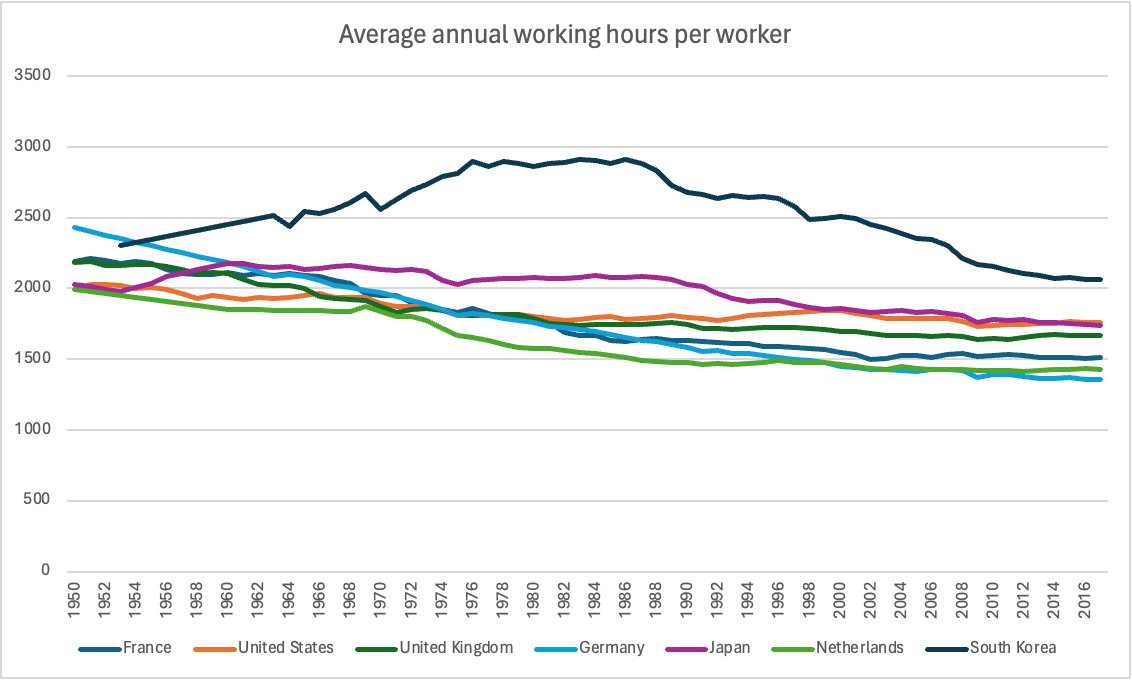

4-hour work week

Maybe it’s because we are all working fewer hours. The 40-hour work week has been the standard since 1932, but the numbers of hours worked has trended down.

Source: Our World in Data based on Michael Huberman & Chris Minns (2007) and Penn World Table 9.1 (2019)

I blame technology, which has made us more productive, and higher household incomes from more female labor force participation. One caveat is that high earners are working more, flipping the long history of lower-wage earners working more hours.

So does that mean eventually we’ll only work 32 hours a week or have a 4-day work week? It was one of UAW’s demands, and people did not even think that was strange. And Bernie Sanders is proposing everyone get one more day off per week—with no loss of pay. That’s the equivalent of a 20% pay increase for the entire economy.

The argument goes we are all so unproductive, depressed, and overworked. So, more time off will lift our spirits and make us more productive. Or we just waste time and can probably do our jobs in 32 hours anyhow. For some jobs that may be true. But others, such as servers, home healthcare workers, management consultants, there is not that much scope for cutting hours.

I do agree more technology will make us more productive. But sometimes that just makes labor more valuable, which increases hours worked—as it has with high-wage workers in the last few decades. It is unclear how it will go.

But mandating a 20% economy wide wage increase now is probably unwise. And in a world where people are waking up to the cost of paying service workers more, it won’t necessarily make people better off.

Until next time, Pension Geeks!

Allison

thank you, I have. more when I was working in industry.

Americans are generally unaware of how much more expensive US medical care is compared to the rest of the developed world while simultaneously the US has the lowest life expectancy in the developed world. The extremely inefficient US healthcare system undermines retirement security because of the excess funding healthcare requires in the workplace and in retirement. Funds that could go towards retirement funding are being siphoned off to healthcare administration costs instead. As a result, the wealthiest country in the world is struggling to fund adequate retirement for its citizens. To put the excess healthcare costs in perspective, the amount Americans pay for healthcare in excess of the rest of the OECD would pay for the US military spending twice over each year.

The real solution to retirement funding is figuring out how to get the US healthcare per capita costs to be in the same general vicinity as the rest of the developed world while hopefully matching those countries life expectancies and medical outcomes. The money that would be freed up would essentially wipe out the funding shortfalls for retirement without any new taxes.