Known Unknowns

Hello,

Welcome to Known Unknowns, a newsletter that likes objective metrics—even if they turn out to be wrong--that's the point.

Chile forces economists to question what it’s all about

The most effective way to increase the odds of a good outcome is to set a clear, well-defined, and measurable goal. When it comes to development (or any kind of) economics, the goal has traditionally been increasing things like GDP per capita or alleviating poverty. By these standards, mainstream economics have done quite well in the last 60 years. But the protests in Chile makes one question if higher living standards is enough.

The New York Times argues that the protests are about inequality, that growth is not enough—it must be equally shared. Many economists now believe inequality causes political instability; thus, the right tax policy needn’t raise revenue as efficiently as possible, it must promote social stability by taxing the bejesus out of the rich.

Color me skeptical. First, I am not convinced that inequality is all at fault here. True, we have more populism/instability and more inequality. But we have other factors that tend to cause social unrest, e.g., things that get less attention and are harder to solve, like more risk and uncertainty and expensive education and healthcare. If you think inequality in-and-of-itself is a problem, then simply making the rich less rich will make the middle class feel better. I am not sure that’s true. It strikes me as a lazy intellectual argument.

Even if it were true, I worry some economists are going somewhere they should not. The good thing about GDP and poverty is that they are easy to measure and justify. How can you measure the right amount of inequality so the middle class does not take to the streets? Or at what level of wealth do rich people not have undue influence on the political process (Clinton donors are outliers, I guess)? It feels like, if righteousness is on your side, people feel like reason, logic, and norms don’t apply to them.

I agree that Chile shows that economists do need to broaden their objectives. But I don’t think the problem is inequality as much as it is insecurity and rising prices. The global economy is in transition, from technology and trade. This has increased living standards but also created more uncertainty. So, instead of obsessing about arbitrary inequality measures, I think a more productive path is to develop risk metrics and then more robust safety nets to address those risks. The benefits need to target the middle class and include job training, better unemployment benefits, wage insurance, universal access to education, and a basic level of healthcare. That’s just to start. Finding the right solution requires identifying the problem, be it economic anxiety or economic resentment—two different problems that take different solutions.

True, we may need to tax high earners more to pay for the programs that will make the middle class more secure. But there is a big difference between increasing taxes with the primary intent of reducing wealth and taxing people just because they can spare more income to pay for useful government services.

I also want to add that I remain a fan of the Chilean pension system, which is one of the best-designed defined contribution schemes out there. Yes, fees were too high and coverage rates are too low (many Chileans are in the informal labor market). But those problems can be fixed—or more easily fixed than grappling with a broken defined benefit system. I hope Chile doesn’t throw the baby out with the bath water here.

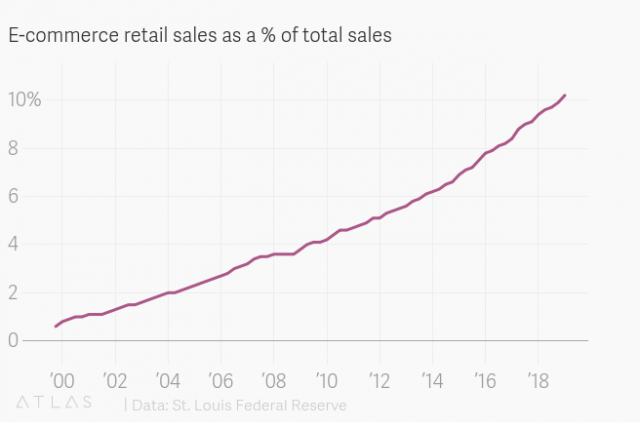

How Amazon changed the economy

I am open to economists redefining their objectives and how they measure success because the world constantly changes and so should our goals. I think reaching higher standards of living is still a good goal, but what we mean by “living standards” may mean more than what we can consume.

It is remarkable how much the world has changed in the last 20 years. The retail experience—which has dominated economic and social interaction for thousands of years—has been totally transformed by Amazon.

For example, prices change more frequently—and are often marked down—because pricing is more competitive. Markdowns have become more frequent than markups. This may be one reason why inflation is so low and why the channels of monetary policy work differently than they did before.

Cheaper and easier access to goods and more transparency appears to be unambiguously good using traditional economic models. And, indeed, there are many benefits: Think of an overworked single mother who can get bulk goods cheap online.

But traditional economic models don’t account for what’s lost, like the social cohesion that comes from an in-person market place, where people interact, or an economy that offers rewards to superstars and makes it harder for the little guy to compete.

Telling better stories

The Washington Post argues that economists need English majors so they have help telling better stories—based partly on Bob Schiller’s new book. I have more to say on his book (saving that for another time), which is less about good storytelling and more about how the power narratives have to shape the economy. But I appreciate the sentiment—it was the idea behind my book. My hope is that good stories can help people understand the value of economic and financial models, which are essentially parables, by retelling them as actual parables.

I have been wondering a lot about how economists can reclaim their narrative. The problem is that economic orthodoxy has been relatively successful, in terms of rising living standards and poverty alleviation. But people connect more to stories of hardship and injustice. Maybe that’s why inequality has been cast as the biggest economic challenge of our time, even if we still have no rigorous estimates of the harm it actually causes.

In other news

Excellent Lars Hansen video or measuring climate risk

Jason Zweig flirts with the fallacy of time diversification

Useful numbers on plans to expand Social Security

Me in Harvard Business Review on how to manage your human capital like a financial asset.

I was on Alan Alda’s podcast. A career high!

Until next time, Pension Geeks!

Allison