Known Unknowns

Hello,

Welcome to Known Unknowns, a newsletter that is coming to terms with uncertainty.

Making sense of markets

We are living in times of extreme uncertainty, or risks that we have no way of measuring. When we can’t measure risk, we can’t manage it—and that explains why the markets make absolutely no sense these days. Sure, we got some good news last week, but considering the long and still uncertain road ahead, it seems like the stock market went up more than we would’ve expected.

I spoke to Zvi Bodie about how to make sense of risk in this new environment. I was recently asked whether the market will be riskier forever more, and I thought it was a strange question, because stocks are always risky. And as Zvi points out, the VIX term structure is downward-sloping. It is normally upward-sloping, because the far future is normally riskier than the near future. But now it is downward-sloping, because markets expect all of this volatility to stabilize in a several months. And I think that’s right. We get more data with each week that goes by, and that means that we move from uncertainty to risk, and the markets will finally start making more sense.

Zvi also reminds us that investing for the long run is not necessarily low-risk, either. A longer investment horizon does lower the probability of loss, but it also introduces more tail risk, since you have the chance of many years of bad returns. I cringe when people say that if you’re young, you can invest in stocks, because it is less risky. And I’m hearing that a lot lately. Tail risk is real—just look at Japan, or look around you at the world we’re finding ourselves in. It does make sense to have more equity and fewer bonds when you’re young, but that’s only because you have so many years of earnings ahead of you.

One silver lining from this period of time is that I hope people will gain a better understanding of risk and uncertainty, and how you can actually manage each of them—to the extent that you are able. Everyone now understands exponential curves, higher-order derivatives, and how limited the models really are when they are estimated with incomplete or unreliable data. One way in which the world is changing is that there is more data to measure risk. I hope we’ll come out of this more knowledgeable about the limits of data and risk-modeling, but also more open to taking managed risks.

Inflation and monetary policy

Unlike 2008, hardly anyone is concerned that all of the Fed’s extraordinary policies will cause inflation. Deflation is actually a bigger worry, since no one is spending money right now. The scope of monetary policy is not to juice spending and growth. Rather, it is to keep financial markets as liquid as possible so that corporations and municipalities can borrow and not go out of business. I have mixed feelings about doing this in the high-yield market, not because of inflation. There is more risk here, and tons of moral hazard. It seems like for years all we heard about was risky leveraged loans in the high-yield market, and now investors and the corporates who ignored all of these warnings are getting this liquidity. There are no good options there, but a very bad one is more government equity ownership of the private sector. This will only prolong a recovery.

But, as a reformed macroeconomist, I’m more interested in the structural changes that alter the path of macro variables. Low inflation has been a mystery for the past few decades. Two reasons why were better anchored expectations from competent, credible monetary policy, and more trade, which meant cheaper goods from abroad.

So, how do these look going forward? I’m not sure that the Fed is as credible as it once was when it comes to inflation. A year from now, when we’re in the midst of a recovery, can you imagine the Fed increasing rates and slowing the recovery if there’s a hint of inflation? I can’t imagine them purposely doing something that causes a dip in the stock market.

And if we do decide that we need less globalization, that we should be less reliant on China, that we should make more stuff here in the U.S. and not have our supply chains tied up abroad, that could also result in more inflation in the medium term. De-globalization means less tail risk if there’s another global pandemic or political incident, but it also means less diversification. That just-in-time production and making use of cheap labor abroad was efficient—and by efficient, I mean cheap. If anything is going to increase inflation over the long run, I’d say de-globalization poses the bigger risk.

Unemployment and debt

It’s hard to come up with good fiscal policy at the best of times, let alone in the midst of a crisis. There are things to like about the CARES Act. Personally, I think it’s better to pay people through unemployment insurance than taking over company payrolls like other countries have done. It’s more efficient and easier to get people money that way. Granted, it hasn’t gone very smoothly so far, but think how much worse it would be if we started a whole new program. It also means that we can better target the people who need money, including contract workers, furloughed workers, and part-timers.

The unemployment numbers are terrible, and they represent the fact that on top of everything else, many households are also facing serious economic uncertainty. And these numbers don’t even include all of the recent graduates who now have no jobs to start. But these numbers also don’t mean what they used to mean. These aren’t people who lost their jobs because their employer went out of business or faced no demand from a recession. The high unemployment numbers reflect deliberate government policy to shut down the economy and pay people through unemployment insurance. When the economy is re-opened, many of these people will go back to work—at least, that’s what we hope.

It might make us feel better to take over payrolls, and unemployment numbers might look better. But that wouldn’t mean that the economy is truly healthier, or that people are more attached to their employees.

I do worry about how the Paycheck Protection Program will play out. If the economy comes back weaker, and an employer then needs to lay off some of their workers, they’ll be on the hook for their loans. It seems like that could create distortions.

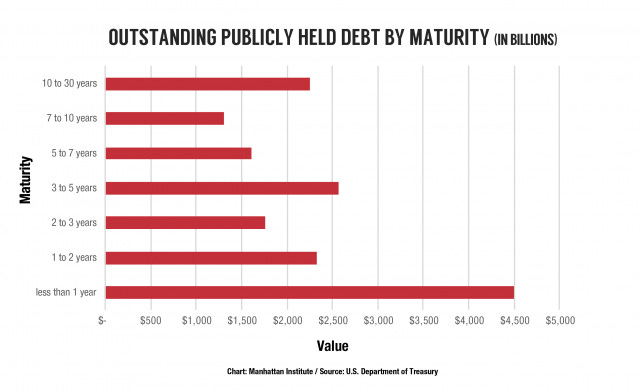

I get the impulse to throw money everywhere now, because we need spending like never before, and rates are low. But remember that we finance our debt with short-term bonds.

That means roll-over risk if rates go up in the future. And they might. This debt will be around for a lot longer than the virus. I agree that now is not the time to be timid, but it’s also not the time to be reckless.

In other (not surprising) news

Public pensions are a white-hot mess

Until next time, Pension Geeks!

Allison