Known Unknowns

Hello,

Welcome to Known Unknowns, a newsletter about the risks we take, in markets and other places, too.

Should People Own More Stock?

It might seem like a really weird time to ask that question. The markets have already experienced a correction and may go lower as the Corona virus spreads. It feels like people have been waiting for a sustained market drop for a long time. When markets are frothy, it doesn’t take much new uncertainty to send them spinning.

It is an unpleasant reminder that the stock market is risky. It is always risky. A steady increase over a decade is not the norm. There is always a risk in risk premium.

Unless things turn around quickly, I expect the Trump administration to scrap its plans to expand stock ownership among the middle and upper-middle class. But I think this is the exact time we should be asking if Americans should own more stock. Most middle to upper-middle earners already own stock; in fact, 80% of American households who earn between $75,000 and $200,000 own equity, usually in their retirement accounts. Among these stock holders, however, the median stock allocation is only 33% of financial assets.

I don’t expect the Trump plan would have increased equity allocations, since it did not introduce meaningful new incentives. But since several Democratic candidates plan to discourage risky assets, it is worth asking if 33% is too low, too high, or just right.

The answer is: It depends on how risky your income is, how correlated it is with the market, your age, and investment goals. But I supposed many Americans could use a little more stock. After all, it is a better investment than housing. And if we are in a new equilibrium where capital offers bigger returns than labor, then expanding equity ownership spreads some the wealth around in a more constructive way than does brute force redistribution.

However, as this week reminded everyone, it also means households will be exposed to more risk. Some people don’t have the temperament, or the financial cushion, to deal with market downturns when a large chuck of their portfolio is at stake. The libertarian in me would like to say “Let them figure it out for themselves.” But people have funny memories when it comes to the stock market; it is easy to forget drops happen until they do. It is not surprising the Trump proposal followed market highs. And we’re not talking about live-and-let-live investing: We are debating tax policy that explicitly encourages or discourages stock ownership.

I suppose I come out on the side of many people could stand to own more stock – but that needs to come with the education of the risks that come with it. After all, there is no shame in risk aversion and avoiding risky assets.

While We Are Asking Untimely Questions

When will bond prices fall?

Everyone is talking about the stock market and finding arbitrary historical comparisons. In case you missed it, then, the 10-year bond hit a record low last week. Less than 1.04%! And that’s nominal. Just when you thought it couldn’t go any lower. I guess small and negative real are better than the alternative.

Yet, I am a little bearish on bonds. I agree they could go even lower. After all, we are the best country and, by that logic, should pay the lowest yields or something. As a pension geek, however, I think long-term. Bond yields are not determined by the Fed; they are set in the market based on supply and demand. Supply is somewhat fixed, unless we elect President Sanders who plans to run VERY large deficits. But, no matter what happens next fall, I expect demand to contract some.

One long-term impact of Corona could be less economic integration – or a decoupling. On a trip to Iowa last week, I met several meat producers who said the virus made them realize how vulnerable they were to the Chinese economy. It turns out they use Chinese chemicals in their meat production (try not to visualize) and are worried what will happen if the disruptions continue and they run through their inventories. They plan to limit their exposure in the future and diversify their chemical suppliers. I suspect they are not alone and that Corona could mean a structural shift in trade flows.

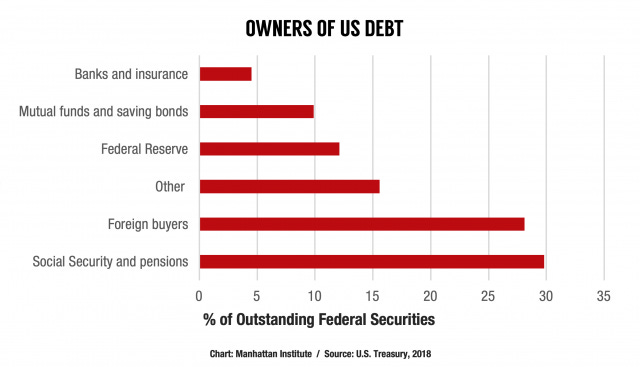

If that’s the case, then China has less need (or ability) to buy US debt. Asian countries are big buyers of US bonds. Less demand and potentially lots more supply means higher yields.

When will this happen? I am too much of an efficient markets person to guess. But I am glad I am not a bond trader. Things could get gnarly.

In Other News

Turns out things like Medicare for All are actually regressive.

Japan explores tontines.

The last risk video Quartz made about my book and other things is out. I love the whole series. It takes something esoteric and makes it relatable.

A slow-moving, systematic risk everyone knows about and choses to ignore.

Until next time, Pension Geeks!

Allison