Allison's ode to the second moment: Tenth issue

Hello,

Welcome to the tenth issue of Allison’s Ode to the Second Moment, a newsletter that shows you can hide risk...but it never goes away.

Turning lead into gold

I initially dismissed it. But it seems to be catching on, even respectable, to argue you can achieve long term, sustainable growth by increasing nominal wages through massive government intervention. The idea is if we pay low-income people more (increase minimum wage and/or massive redistribution), they spend more of their income than rich people, and voila ---you’ve got growth by boosting demand.

First of all, if that were true rising income inequality would’ve produced more saving. But the opposite happened. Consumption as a % of GDP increased, even while the rich got richer and supposedly spent too little.

The demand/spending growth idea seems based on the assumptions that the world will end tomorrow, there exists no risk or uncertainty, and people don’t respond to incentives. Sustainable growth comes from creating value. And this plan simply moves money around, converting savings/investment (which fuel long term growth) into current consumption. It also risks distortions which can have unintended consequences.

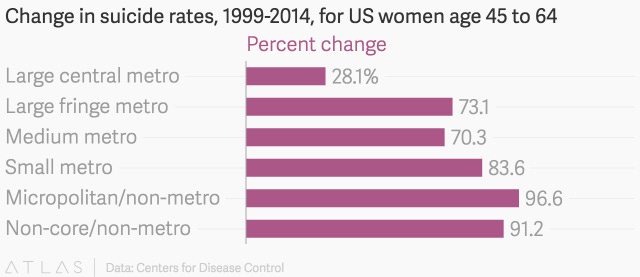

Is a bad economy driving people to suicide?

There's been an increase in suicide rates in America, especially among women in rural areas.

There exists a temptation to blame the economy (inequality, stagnant wages, and instability) for everything terrible these days. Indeed, economic concerns are a factor in more suicides. But mental health and isolation are still the main reasons. We need to understand why people feel more isolated and how economics makes already vulnerable people more susceptible.

Woulda Coulda Shoulda

A study from Brookings looks at what would have happened if the Social Security Trust Fund were invested in stocks instead of treasuries. If only…the Trust Fund would be $1 trillion bigger today and there’d be less of a pressing need for tax increases and benefit cuts.

We already missed that opportunity. But perhaps we can learn from what might have been. Assuming we can reform entitlements and build up a new trust fund…would investing it in stocks be a good idea? Maybe, but I worry about risk. We don’t know how such a large inflow of capital into the market would impact stock prices and the macro economy.

Over time stocks may beat bonds, but stock returns are positively correlated with wages. That means the stock market would tank (and deplete the trust fund) at the same time tax revenues would shrink. There may be upside, though it comes with more risk than meets the eye.

Rebel actuaries never say die

I am still keeping score on the nerdiest rivalry in the world; the one between financial economists, who think pension discount rates should reflect risk, and actuaries, who think discount rates should be the expected rate of return on assets.

Some actuaries went rogue, formed a task force, and wrote a study arguing discount rates should reflect risk. Last week the task force was suddenly and unceremoniously disbanded. And the report will not see the light of day!!!

Actuaries 1

Financial economists 0

For now, anyway…we may have lost the battle, but not the war.

The people who really lose here are pensioners (who count on the promises made to them) and tax payers (forced to make up the difference). Look no further than the Central States multi-employer plan, which is running out of money and options. That’s what happens when we enable risk-taking and over-optimistic projections.

The question of our time

Speaking of low rates causing trouble, there’s some debate on why rates are so low. Are they naturally lower in the post-crisis economy, is there too much money sloshing around looking for a risk-free home, or can we blame central bankers for keeping rates artificially low and causing bubbles? A new paper from the Bank of International Settlements agrees the natural rate is lower, but not as low as people think. They blame central bankers for keeping rates below their natural rate. Some people might think that isn’t so terrible; when they hear low rates they think demand-boosting expansion. But us pension geeks think “oh dear…those pension promises just got a lot more expensive.”

Until next time, Pension Geeks!

Allison