A new game is coming to town

Too bad about the binding budget constraint

Photo by Markus Spiske on Unsplash

Hello,

Welcome to Known Unknowns, a newsletter that, in times of change, aims to find more upside than down.

New President and a Rate Cut!

I love Presidential election day; I wish we could do it every year. Even if the candidate I voted for doesn’t win, it’s thrilling to watch the results come in—knowing the entire country (and even the world) is tuned in to the same event. You can’t take that joy away from me. I think you can hear my enthusiasm on the Reason podcast I recorded that evening before the results were announced—or maybe it was the MAGAritas I’d just had!

I’ll leave the post-mortems to the political experts, but I find it fascinating that so many young people—especially men—swung Republican. Young people are typically reliably left-leaning before they start paying taxes. I suppose the signs were there, with polls worldwide showing young men becoming more conservative. It may be cultural; the left did seem to like men very much lately, and perhaps they didn’t like them back. It seems obvious, but genuinely liking the voters you need is important.

In my Bloomberg piece, I argued that economic reasons also played a role. Young men face very real economic challenges—lower labor force participation, stagnant wages, and an economy where job growth is concentrated in sectors they traditionally don’t enter, like caregiving or education. However, young men saw some economic improvement during Trump’s previous administration, while the Biden-era recovery seemed to benefit women more. This may not have been deliberate policy choices, just the nature of the post-pandemic economy. But men saw some improvement under Trump, and just treaded water with Biden.

Trump has an opportunity to build a truly inclusive economy—one where everyone, including men, can thrive. He could reform the labor market to make it more dynamic and flexible or continue imposing tariffs to revive manufacturing. If he chooses the former, he could convert a generation to the Republican Party.

Our Last Big Debt Bonanza

I expect a lot will happen in 2025. Trump has a significant mandate and potentially both houses of Congress. I foresee many tax cuts, with all TCJA provisions becoming permanent, corporate taxes dropping, and various activities being deemed worthy of tax exemptions. But this could be the last hurrah for our low-tax, high-spending economy. Over the past 30 years, taxes have only gone down as government spending has grown. This trend felt sustainable partly because interest rates also declined, allowing us to believe that debt could rise indefinitely without raising rates. Call it the privilege of being the world reserve currency or safe asset of whatever you want, but it convinced many people that debt had no limit, and the link between debt and higher interest rates was broken, at least for America.

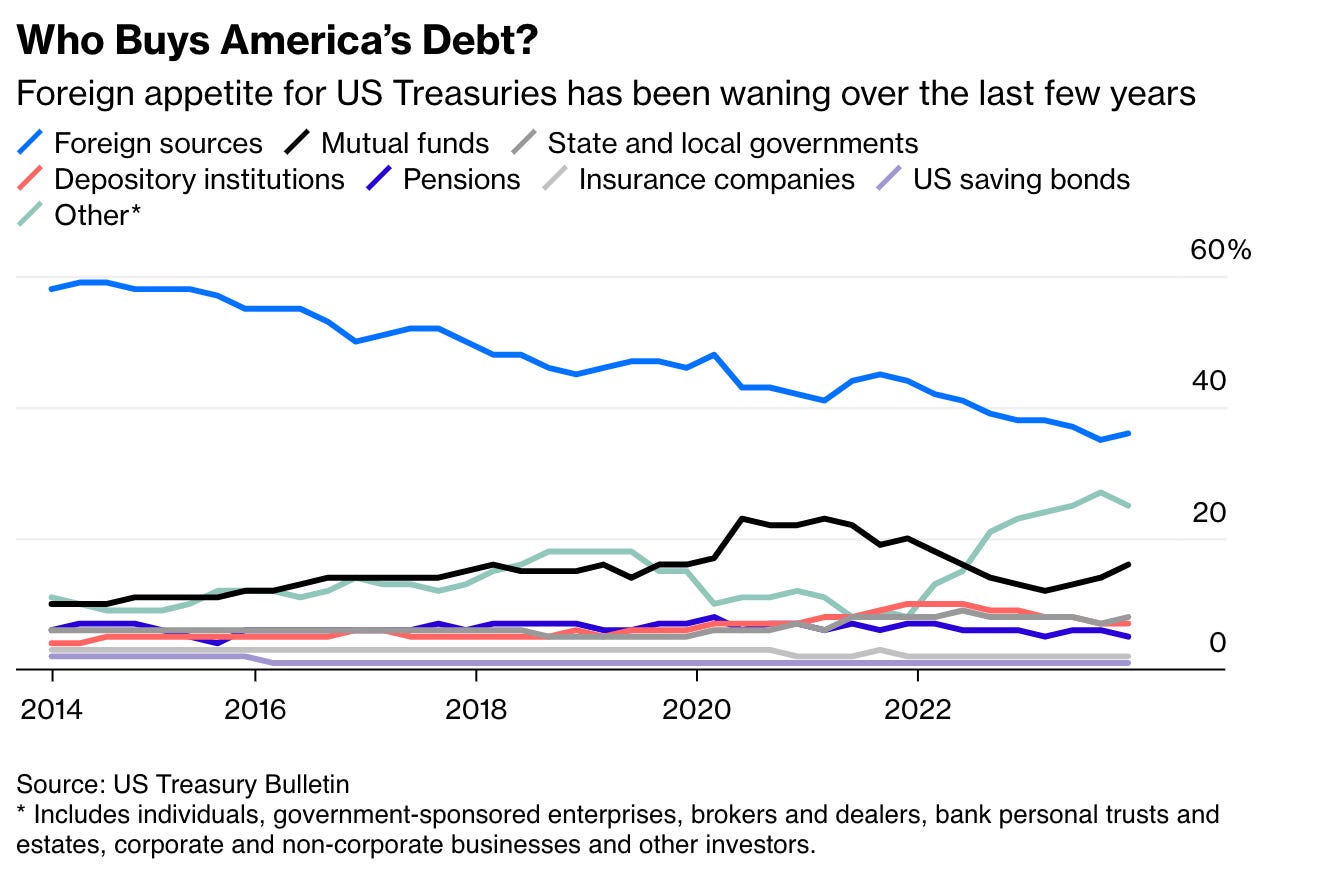

But now winter is coming for the bond market. While I don’t anticipate a full-on debt crisis, we’re already seeing long-term rates tick upward. We’re dealing with a different population of bond buyers now, as foreign governments are less inclined to purchase U.S. debt at any price. The new buyers demand higher yields and won’t accept debt and inflation risks without adequate compensation.

As rates rise, interest payments consume a larger share of the budget, forcing tough choices. I wouldn’t bet on a smaller government; everyone—not just the wealthy—will likely face higher taxes. I am rooting for a VAT.

I appreciate the Trump team’s confidence that higher growth will offset these costs, and I agree that some of their policies could boost growth. However, expecting enough growth to cover existing and future debts, including the entitlement bomb approaching, is overly optimistic. Achieving the necessary growth is even more challenging with an aging population and higher interest rates. It would take a significant transformation to reach that level of growth.

Perhaps we’ll see it—or, at the very least, I hope for structural reforms that overhaul our regulatory environment, helping the economy flourish regardless of future administrations. I had a lively debate on this topic on CNBC last week.

Until next time, Pension Geeks!

Allison

he won't. no one has the bravery to curtail spending. the reason we have a revenue problem is our spending problem!!

It will be interesting to see whether there is any fiscal stimulus beyond extension of the tax cuts, which would keep the status quo. The reconciliation rules state that beyond ten years any bill has to be neutral in terms of the deficit. So if the 2017 tax cuts are made permanent, I'm not sure what the offset will be beyond ten years. Maybe they will have to sunset again. There's also the question of inflation, which proved to be a political killer of whoever presided over it. If you're a Republican Senator up for re-election in 2028 or 2030 post-Trump, you might fear inflation more than you fear Trump.