Economic policy gets weird

Economic policy gets weird

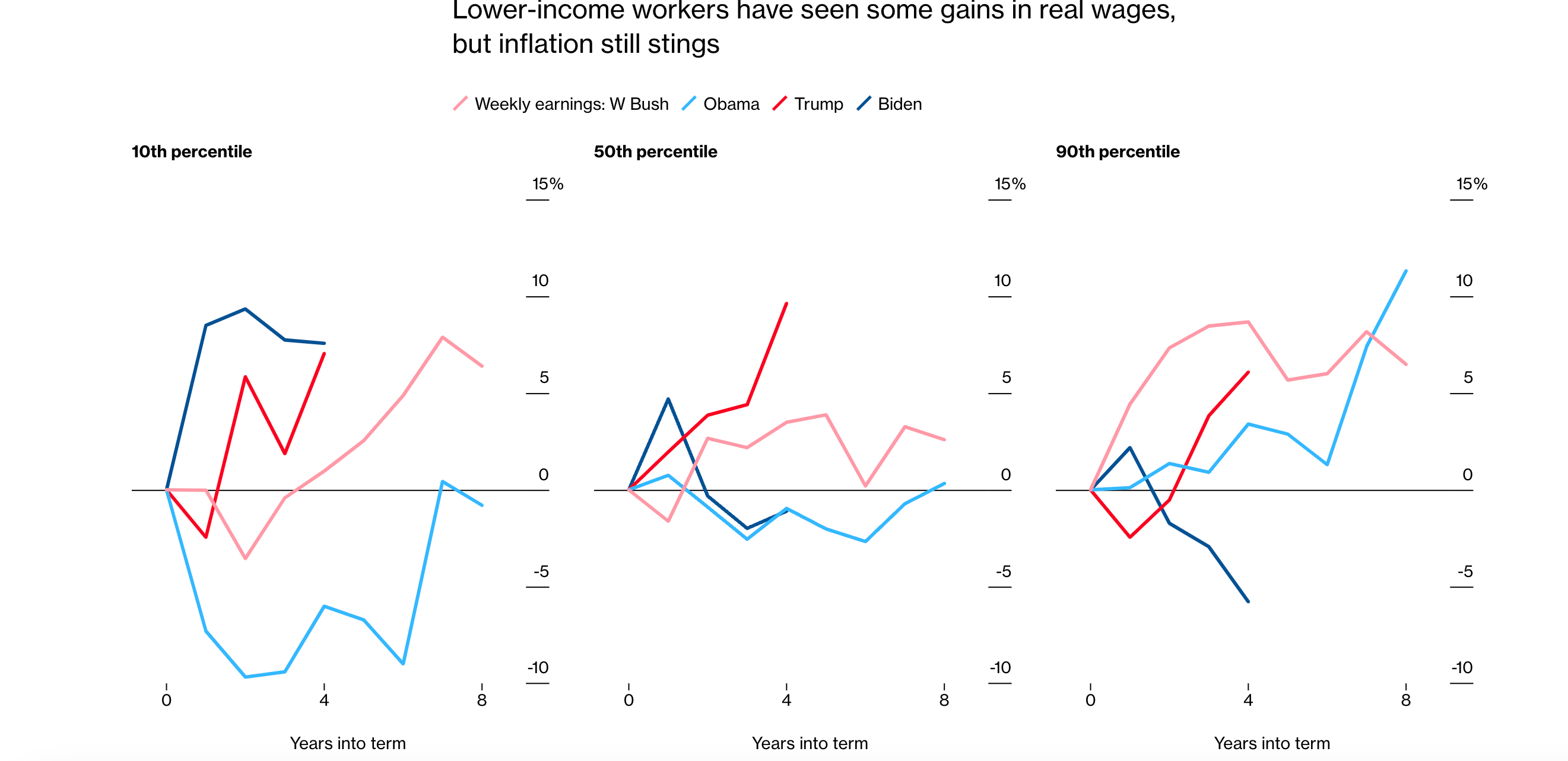

And real income still has not recovered

Photo by The New York Public Library on Unsplash

Hello,

Hello,

Welcome to Known Unknowns, a newsletter that remains hopeful even bad economic ideas can eventually lead somewhere good.

Weird Times

This is a strange election for many reasons. I’ll leave it to the experts to discuss polling, political maneuvers, and their implications. But the economics? Well, it's just plain weird. There are a few fine ideas—I'm all for helping small businesses—but the rest, well, it’s what happens when you have lawyers setting economic policy.

First, there was the tax on tips, which seemed too crazy to be true—just something said at a campaign event—but now both sides have embraced it. Then there are the tariffs, the anti-price gouging rules, and the rent control. And there's even a plan to give people money for a down payment, but without any credible way to increase housing supply. It’s all so bad.

But there are a few bright spots. I was heartened when, in the early moments of the debate, the candidates discussed whose policies economists hate more. That at least suggests some interest in what we have to say.

The latest idea is that overtime might also be exempt from taxes, which makes no sense. When I want to feel optimistic, I tell myself that between exempting all sorts of income from taxes and increasing tariffs and subsidies (which are essentially the same thing—don’t let anyone tell you otherwise), we are, if you squint hard enough, moving toward a world where we tax consumption rather than income. And that’s the world I’ve always wanted. Of course, we’re doing it in the worst possible way—distorting behavior by taxing foreign goods more than domestic ones and taxing certain kinds of work more than others. All of it is very, very bad. But still, we should be taxing consumption more than income. Maybe this is a step in that direction. Probably not—I’m trying too hard to be optimistic. Sometimes, the journey is so bad the destination isn’t worth it.

I wrote for City Journal about the idea of launching a sovereign wealth fund, which is probably our least-bad, bad idea. Trump floated the idea, but apparently the Biden administration had already been working on it. The concept is to use revenue (likely taxes or money from energy sales—though money is fungible, so it doesn’t really matter) to invest in things the government thinks we need. They’re confident these investments will pay off big and compensate for the debt we’ll incur. This is otherwise known as a leveraged bet—what could go wrong?

I argue that we already have sovereign wealth funds—many of them, in fact. They’re also known as public-sector pension assets. Their track record doesn’t bode well for taking leveraged bets with taxpayer money. After the Central States bailout—the massive multi-employer pension plan rescue that most people probably missed because it happened during the mid-pandemic spending bonanza (unless you read this newsletter closely, in which case you’re still as mad about it as I am. For new subscribers: we bailed out a miss-run, underfunded pension with pretty much the only condition being they’d never, ever cut benefits)—the federal government has effectively guaranteed public pensions, too. Can we bail out the Teamsters but not retired teachers and firefighters? Of course not.

TL;DR: We already have a sovereign wealth fund, because we’re on the hook for more than $5 trillion worth of them.

Why People Like Trump

There are cultural reasons people like him. But when people say the economy was better under Trump, I think they mean their pay went up while he was in office. Bloomberg updated its Biden-metrics feature, which shows various economic indicators under different administrations. I focused on inequality. What struck me was that real income spiked in 2020 and then fell for nearly everyone except the lowest earners. Most Americans have lower real incomes today than they did in 2020 and 2021. And that’s the bottom line: inflation made people poorer and introduced more risk into their lives. Nothing else matters—not the stock market, not the low unemployment rate, not the new factories built, and not the saving democracy thing. Many American households are either worse off or just getting back to their pre-pandemic income levels.

It’s telling that so much has been written in recent years about the question, 'Why aren’t people enthusiastic about this great economy?' yet the answers rarely mention the fact that real incomes are lower. I’m not sure why this is. Perhaps many pundits (including trained economists) and journalists were unaware of the income data, or maybe they simply believed what they wanted to believe

What was also striking is that the Trump administration was the only recent one where all income groups experienced real wage increases throughout his term. That probably explains why people believe he was better on the economy.

I don’t entirely blame or credit either administration for these trends. The Trump tax cuts helped somewhat, but I think real income growth under Trump was mostly due to where we were in the business cycle and an overdue recovery from the 2008 recession. But voters don’t care—rightly or wrongly, presidents get credit for the economies they preside over, even if they don’t control them much.

By the same token, Biden has implemented some policies that worsened inflation, but much of the inflation would have occurred regardless. If Trump had won in 2020, his time in office probably would have coincided with a fall in real income, too. In fact, I recall that in 2020 Trump supported many of the same bad policies (like sending everyone checks in 2021) that contributed to inflation.

Why is it that the only thing we have bipartisan consensus on is bad economic policies?

Until next time, Pension Geeks!

Allison

Well said! Public understanding of basic economics is terrible and sad.

This campaign seems to be about dueling handouts with literally no mention of our unsustainable debt and deficits by the media or the candidates. Fantasyland.

Hey- we have 2 pct growth and all it takes is 6 pct of GDP deficits at full employment and a price level 30 percent higher than 5 years ago in many products. Who knew it was so easy? As long as we can borrow and spend another 6 or 7 percent of national income every year we can grow nominal national income by 4 or 5 percent a year. Like a magic money tree (for those who can’t do the math).